How to Choose an English-Speaking Financial Advisor in France

Finding a reliable English-speaking financial advisor in France can be difficult, especially when you are dealing with a new tax system and unfamiliar rules.

Moving to France is a dream for many, but once you are settled, the real challenge often begins: retirement planning, structuring your investments, and handling cross-border questions require clear decisions from the start.

In this context, you need more than basic advice: you need a trusted partner who understands both your language and your situation.

📌 What to look for when choosing an English-speaking financial advisor in France :

- Quick wins an experienced advisor can deliver : a more tax-efficient portfolio structure and proper reporting of foreign accounts.

- What to look for : a direct, client-paid model (MiFID II standard), ORIAS registration, and proven experience working with expatriates in France.

- Questions to ask your advisor : “Do you receive commissions from the investments you recommend?” and “Do you regularly advise expat clients in France?”

If you want independent advice with open‑architecture options and expat expertise, you can book a video consultation with a Prosper Conseil wealth manager here.

TABLE OF CONTENTS

- Why expatriates in France need an English‑speaking financial advisor

- How to choose the right financial advisor in France

- Prosper Conseil: a good fit for English-speaking expats in France?

Why expatriates in France need an English‑speaking financial advisor

🧭 When you manage your money as an expat, the real challenge is not only finding the right investments, but also understanding how everything works together.

In France, two people with the same asset allocation can end up with very different results. This is because taxes, investment structures, and account types all have a direct impact on what you actually keep after tax.

Financial advisor in France: navigating a unique and complex tax system

⚙️ The French tax system is not always intuitive. Each type of income follows different rules, and small mistakes can cost money.

For example:

- Salary and dividends are taxed in different ways.

- Some income is taxed at progressive rates.

- Others may be subject to the « flat tax » or additional charges.

📌 In France, you often have to deal with two layers: Income tax (impôt sur le revenu) + Social charges (prélèvements sociaux).

There are important differences between countries and they often come as a surprise when you move to France :

- Some countries tax you even if you live abroad: in certain cases, you may still have to report your income in your home country, even while living and paying taxes in France. This is notably the case for US citizens, who must declare their worldwide income to the IRS regardless of where they live.

- France has its own investment structures (often referred to as “investment wrappers”, such as assurance vie, PEA, PER): these are the main investment frameworks designed for French tax residents. They offer specific tax advantages, but only if you actually use them.

💡 In practice, many expats keep their existing accounts abroad… while overlooking the tools that are actually optimized in France.

Cross-border financial challenges

🌐 As an expat, your finances are often spread across countries.

This makes things more complex, especially when rules are different in each country.

Common situations include:

- Income coming from different countries.

- Bank or investment accounts abroad.

- Foreign pensions (UK, US, etc.).

📌 France requires you to declare all foreign accounts every year. Even if you do not use the account, you still need to report it. Not declaring a foreign account can lead to a €1,500 fine per account, per year. This is a simple rule, but many expats miss it.

Pensions can also be tricky. Depending on the situation, they can be taxed in France, abroad, or both.

💡 In this context, having a financial advisor who speaks English can make a real difference. They can help you avoid costly mistakes, and structure your finances in a way that is both compliant and efficient in France.

Risk of costly mistakes without proper advice

➡️ Common mistakes we see among clients who have moved to France:

- Keeping foreign structures that no longer work in France.

- Choosing the wrong tax-efficient structure in France.

🔎 Example: an expat who previously lived in the UK keeps their investments in a standard brokerage account (like a GIA, similar to a French compte-titres). When this expat became a tax resident in France, all foreign investment income (not only dividends but also interest and capital gains on sales) became taxable in France.

If the same investments were instead held within a French « assurance vie » or « plan d’épargne en actions » (PEA), taxation could be significantly reduced and deferred over time.

The underlying investments may be identical, but the tax treatment is completely different. And over the years, this gap can become substantial.

💡 Note: The French tax system is complex, and small structural decisions can have a big impact over time. A well-designed strategy combining the right investment wrappers can significantly improve outcomes without increasing risk.

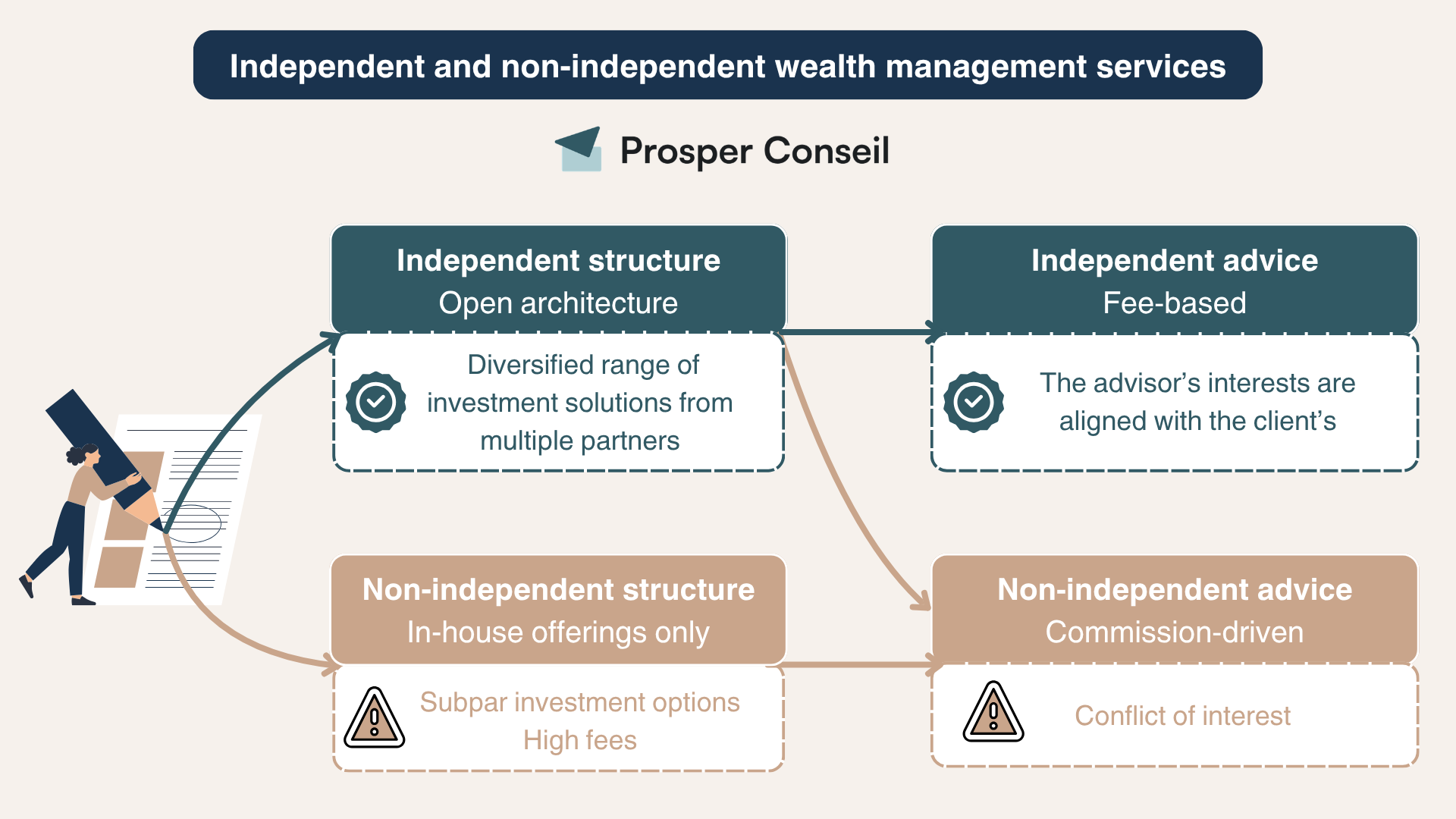

How to choose the right financial advisor in France

When you are an expat, choosing a financial advisor is not just about language.

A truly independent advisor helps you avoid costly mistakes, while a commission-driven advisor may, in contrast, push in‑house solutions that aren’t the best fit.

The diagram below summarizes the two approaches: open‑architecture, fee‑based consulting (independent) versus in‑house, commission‑based offerings.

We can now look at the concrete differences between independent and commission-driven advice, so you can choose an advisor who genuinely acts in your best interest.

Independent vs non-independent advisors (key differences)

Not all advisors offer the same quality of advice. The crucial differences are how they are remunerated and which solutions they’re allowed to recommend.

Independent advisors

Two pillars define true independence as a financial advisor in France:

- Independence (open architecture): an independent advisor is not tied to any bank or provider. This means they can select the most relevant solutions available on the market, based solely on your situation.

- Direct client‑paid model (MiFID II standard): they are paid exclusively by the client, under transparent terms agreed in advance, like lawyers or accountants. No commissions. No retrocessions. No hidden incentives.

This alignment is crucial: your interests and your advisor’s interests are strictly aligned.

💡 Note: this is the model we apply at Prosper Conseil. Among independent advisors in France, less than 10% operate under this strict client‑paid model.

Non independent advisors (the hidden trade-off)

Many advisors, especially those working in banks or large networks, may seem free at first glance.

But this is where the illusion of free advice comes into play:

- They are paid through commissions embedded in the investments they recommend.

- These commissions can be significant (entry fees, ongoing fees, incentives).

- This creates a conflict of interest: the advisor may favor products that pay them more.

If you are not paying for the advice, you are often paying for the consequences.

💡 Note: There is no free lunch: if the advice is free, you are the product.

Checklist for choosing a good financial advisor in France as an expat

📌 Choosing the right advisor is like choosing a co-pilot: you stay in control, but you need someone who knows the route and the risks.

Here is a practical checklist you can use to choose a good financial advisor.

✅ Fluent English communication

This goes beyond basic fluency:

- Can the advisor explain complex topics clearly in English?

- Can they write reports and strategies without ambiguity?

In cross-border situations, misunderstandings can quickly become expensive mistakes.

✅ Transparent fees (no hidden commissions)

Ask one simple question: « How exactly are you paid?”

You should get a clear and precise answer:

- Fixed fee.

- Percentage of assets.

- Any indirect compensation.

If the answer is unclear, you are likely facing the illusion of free advice.

💡 Note: A very common situation we see is an international client going to their bank with significant wealth, being redirected to in-house products they don’t fully understand. In the end, they often hold layered products with entry fees, ongoing charges, and limited transparency.

✅ Regulatory status (ORIAS, CIF…)

In France, a legitimate advisor should be properly registered.

Check for:

- ORIAS registration.

- CIF status (Conseiller en Investissements Financiers).

This ensures a minimum level of competence and protects you as an investor.

✅ Experience with expat clients

An advisor used to working with expats will already know:

- Common mistakes (undeclared accounts, wrong tax structures…).

- Administrative constraints.

- Cultural differences in investment habits.

This experience helps you avoid costly trial-and-error situations.

Prosper Conseil: a good fit for English-speaking expats in France?

At Prosper Conseil, we support expatriates with a clear objective: help you build a structured, efficient and easy-to-understand wealth strategy within the French system, while taking into account your international situation.

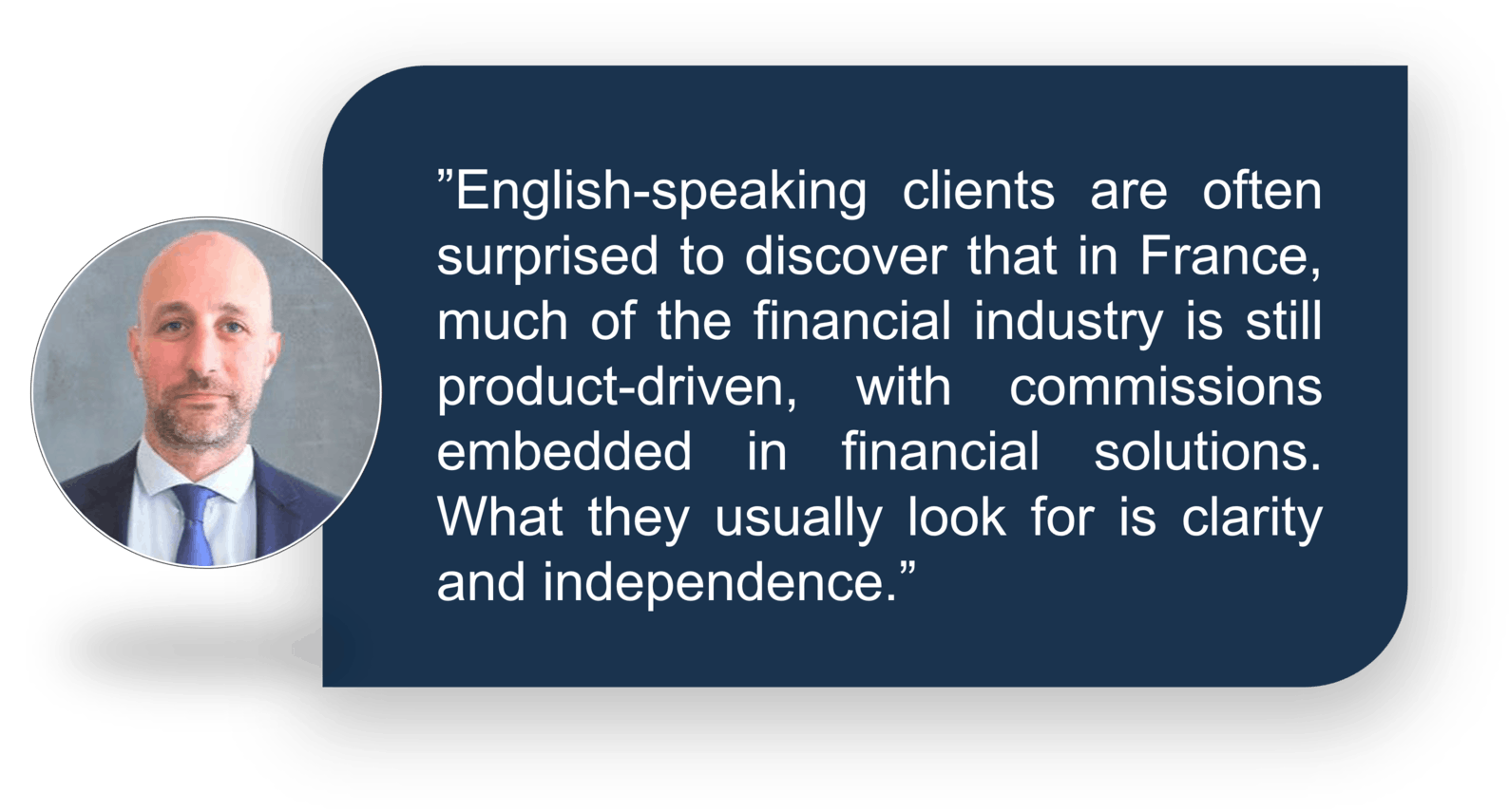

Matthias Michelin, General Manager & Wealth Manager at Prosper Conseil :“What usually makes the difference when clients come to us is simplicity and alignment. We focus on clear, efficient, and cost-effective solutions using straightforward asset classes such as ETFs for equities, bonds, gold, private equity, or real estate. All of this is structured within a global allocation approach that clients can actually understand.”

Our independent model (no commissions)

For expatriates, an independent financial advisor in France makes a real difference.

🧭 Rather than focusing on what to invest in, we focus on how to structure your wealth globally:

- Align your investments with your French tax residency.

- Avoid mismatches between foreign accounts and French taxation.

- Select cost-effective solutions, such as low-cost index funds.

- Ensure consistency between your liquidity needs and long-term objectives.

How working with Prosper Conseil unfolds: a clear path for expats in France

At Prosper Conseil, we follow a simple and structured approach to help you move from uncertainty to confident decision-making.

- We begin with a preparatory wealth assessment, a dedicated consultation where we step back and analyse your full situation: income, assets, tax residency and international constraints. This first step allows us to identify the key optimisation opportunities.

- If we move forward, we then build your personalised financial strategy. This includes selecting the right investment wrappers (assurance vie, PEA, brokerage accounts), defining your allocation, and structuring your investments in a tax-efficient way. Most importantly, we guide you through the implementation.

- Finally, we ensure ongoing monitoring and adjustments over time. Your life evolves, markets move, regulations change. Our role is to help you adapt your strategy when needed, and avoid costly mistakes driven by short-term reactions.

At each step, the objective remains the same: give you a clear framework to make better long-term financial decisions. All our advice is delivered entirely through individual video consultations, which means we can support you wherever you are in the world.

➡️ If you would like to get started, you can book your first consultation with an English-speaking financial advisor at Prosper Conseil here

Plus de patrimoine,

plus de revenus,

moins d’impôts !

Un conseil global à 360° pour mieux

profiter de votre patrimoine